Articles

Inflation: A Way Forward

After a long hiatus, inflation has made quite a comeback in everyday lives of consumers around the world. Generally defined as the increase in the prices of goods and services in an economy, inflation had been below historical averages most of the past decade, with the backdrop of a longer-term decline since peaking in the early 1980’s. The COVID-19 pandemic was the catalyst for a revival, initially due to constraints on supply chains and global trade. However, as economies globally recovered from the pandemic, inflation readings continued to show signs of growth.

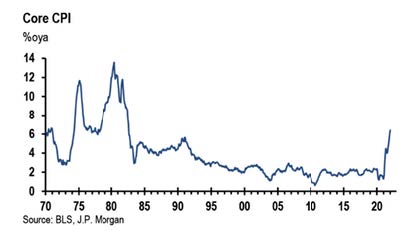

The phenomenon was initially described as “transitory” by economists and investors, believing that inflation would slow as supply chains and global trade healed. This assumption proved to be incorrect, with the “transitory” description has been dropped since mid-2021, as all major measures of inflation have continued to increase at a consistent and rapid pace. The most commonly referenced inflation measurement, the Consumer Price Index (CPI), is tracked including food and energy prices (headline CPI) and excluding food and energy prices (core CPI). The reading through February showed that compared to one-year ago, headline CPI rose +7.9% and core CPI rose +6.4%, the highest level in almost 40-year for both readings. Importantly, this reading does not account for the subsequent increase in energy and other commodities after the escalation in Ukraine.

Inflation is an impactful force to the global economy and therefore financial markets; the sharp increase certainly has the attention of policymakers. In the United States, the Federal Reserve operates under a “dual mandate” of “price stability and maximum sustainable employment”, with the former goal referencing inflation. Due to the improvement in the labor market, and consistently high inflation readings, the Federal Reserve is expected to raise interest rates starting in the March meeting. The first increase will mark the start of tighter monetary policy, which will influence equity and bond markets in the short-term. The additional unknown duration of the supply disruptions in the oil and gas market will also muddy the waters for policymakers over the coming months.

The long, secular decline in inflation readings is over in the short-term. With inflation readings already near 40-year highs prior to the conflict in Ukraine, the response by policymakers over the coming months will be widely followed by investors. As we transition to a rate hiking cycle and inflation stays firm, the environment will likely require investors to shift their approach. Looking back historically over periods of rising inflation, asset classes such as commodities, real estate, value equities, US small cap equities and international equities tended to do well. Within equities, dividend paying stocks may offer an attractive opportunity for investors seeking growth with income in an inflationary environment. One additional portfolio consideration for investors: inflationary periods have had implications for the relationship between stock and bond returns, with high and rising inflation historically reducing the diversification benefit from bonds (positive correlation between stocks and bonds). While the approach may be different than the past 20 years for investors, there are likely to be opportunities for long-term investors to take advantage of as we navigate the ever-changing investment environment.

Views and opinions expressed are current as of the date of this white paper and may be subject to change; they are for informational purposes only and should not be construed as investment advice. Prior to making any investment decision, you should consult with your financial advisor about your individual situation. Although certain information has been obtained from sources considered to be reliable, we do not guarantee that it is accurate or complete.

Forecasts, projections, and other forward-looking statements are based upon current beliefs and expectations. They are for illustrative purposes only and serve as an indication of what may occur. Given the inherent uncertainties and risks associated with such forward-looking statements, it is important to note that actual events or results may differ materially from those contemplated.

Confluence Wealth Services, Inc. d/b/a Confluence Financial Partners is an SEC-registered investment adviser. Registration of an investment adviser does not imply any level of skill or training. Please refer to our Form ADV Part 2A and Form CRS for further information regarding our investment services and their corresponding risks.

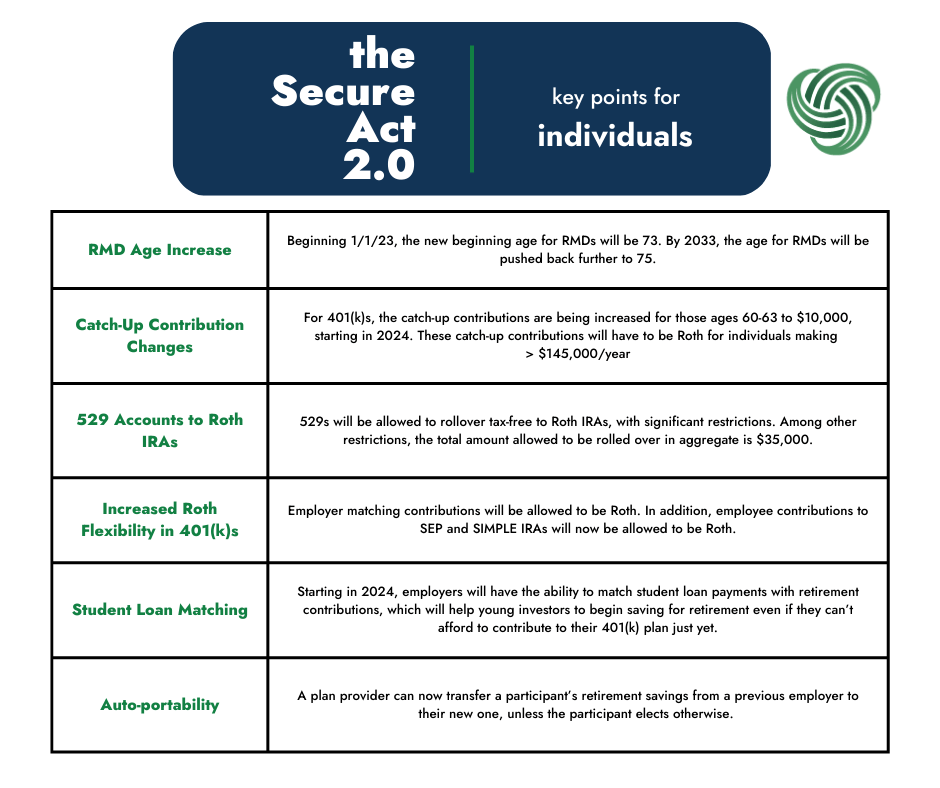

In late December, a $1.7T omnibus spending package was passed in Congress and subsequently signed into law by President Biden. This bill included some significant updates to the landmark 2019 SECURE Act, such that this portion of the legislation is being referred to as SECURE Act 2.0.

While there are many important updates in the law, I’d like to focus on two items that we believe are especially significant

This means that investors who will turn 72 in 2023 received a pass on what would have been their first RMD! It also means that the window of opportunity for income planning in retirement is extended.

Some of the most opportune years in terms of income planning are the years between retirement and when RMDs begin. In these years, individuals tend to be in a relatively low tax bracket, because they no longer have high employment income and they also don’t yet have required income coming from their retirement accounts.

If these retirees are able to live on Social Security and income from taxable brokerage accounts, they could end up in an unusually low tax bracket. These years can then be used to “harvest” capital gains at a 0% tax rate, or convert portions of a traditional IRA to a Roth IRA. The lower adjusted gross income can also help retirees save on things like Medicare and Social Security taxes.

The total amount allowed to be rolled over in aggregate is $35,000, and the rollovers must be done in accordance with the annual Roth contribution limits (currently $6,500 for those under age 50). In addition, the 529 must have been established for at least 15 years.

This change will help to alleviate investor fears of what may happen to 529 funds if the beneficiary chooses not to pursue higher education.

The change also allows for a strategy whereby investors begin planned rollovers to a Roth IRA once the beneficiary turns 16. At today’s limits (which will be adjusted up for inflation), a 529 beneficiary could have $35,000 plus earnings saved in a Roth IRA before graduating from college. That is a solid head start!

If you have questions about how these opportunities could affect your financial planning, please call one of our offices to speak with a wealth manager today.

See below for additional key provisions in SECURE Act 2.0:

732 E. McMurray Road, McMurray, PA 15317

From rebate checks to small business support, there is quite a bit packed into the Coronavirus Aid, Relief, and Economic Security (CARES) Act that was signed into law on Friday. The $2+ trillion emergency fiscal stimulus package is intended to mitigate some of the economic effects caused by the COVID-19 outbreak.

We have all been working to gain an understanding of the law so that we can act as a resource for our friends and family looking to take advantage of the applicable provisions. We have been reading numerous articles, participating in webcasts hosted by industry experts and large accounting firms, and talking with banks to understand the process for various provisions. New information is still coming out daily, but please do not hesitate to use us as a resource as we work through this pandemic.

Here is a look at some of the key provisions in the CARES Act that may be of interest to you:

What’s next? Treasury Secretary Steven Mnuchin has targeted early April to deliver the funds. Discussions are starting in D.C. around a possible next phase of economic relief, although it’s just talk for now.

We’ll continue to keep you updated with relevant and timely information. In the meantime, please don’t hesitate to reach out. These are difficult times in which we are living, but we are confident that we will get through them together.

We are happy to announce Confluence Financial Partners has been named as one of Pittsburgh’s Best Places to Work by The Pittsburgh Business Times.

The 2019 Best Places to Work in Western Pennsylvania honors the region’s most outstanding workplaces. Winners are selected based on an online employee survey in June of this year and are honored at an event and in a special section of the paper. You must have at least 10 employees working in western Pennsylvania to participate. (Anyone with 5 percent or more ownership in the company may not participate in the survey and does not count toward the final employee total.) Companies do not have to be based in western Pennsylvania. Only employees working in the region are included in the survey and results.

Confluence Financial Partners is pleased to announce the hiring of Loren Paul Fiffik. He will serve as Wealth Manager working out of our Pittsburgh location. Loren is a Certified Financial Planner (TM) and comes to us from PNC Investments.

We are pleased to announce the hiring of Nathan R. Garcia. He will serve as Wealth Manager working out of our Pittsburgh location. Nathan comes to us from PNC Investments with 18 years of experience in the financial services industry.

Neil Rongaus, Wealth Manager for Confluence Financial Partners of Southpointe, grew up in Donora, PA where he attended Catholic School through fifth grade and continued his middle and high school education in the Ringgold School District. In 1997, he earned his degree in Finance from Duquesne University. Rongaus now resides in Carroll Township with his wife Marijo; son Marco (8); and daughter Remi (5).

The associates of Confluence Financial Partners chose to “Go Red” every Friday during February in support of the American Heart Association’s campaign bringing awareness of women’s heart health to the forefront.

Confluence Financial Partners Wealth Manager, Mark Eckels, his family, friends and home office coworkers participated in the Tampa Bay Heart Walk alongside Raymond James Chairman and numerous other corporate sponsors to support this worthy cause.