Articles

Reflect, Plan, Measure: Let’s make 2024 great!

The beginning of a new year is an exciting time to reflect, dream, and plan for the future. January is a month filled with anticipation and the good news is that we have control over 2024 and we can be the architects of our year.

To do so effectively, we need to do 3 things:

By implementing the Reflect, Plan, Measure framework, we will become active participants in the creation of a year filled with intention and excitement.

Great Days Ahead!

When someone thinks about socking away money in a college fund for children or grandchildren, the first thing that comes to mind is a 529 plan – a savings plan for qualified educational expenses, which may include not only tuition, but also room and board, books, and other school supplies. But did you know that a 529 can also be an attractive consideration for transferring generational wealth?

The Basics:

The Advanced:

Whether you want to reap the ‘basic’ benefits of a 529 savings account, or want to discuss the ‘advanced’ benefits – the best approach is reaching out to your Confluence Wealth Manager or starting the conversation altogether. We look forward to helping you and your family with education planning in 2024.

Month in Review

Narrow Market Leadership

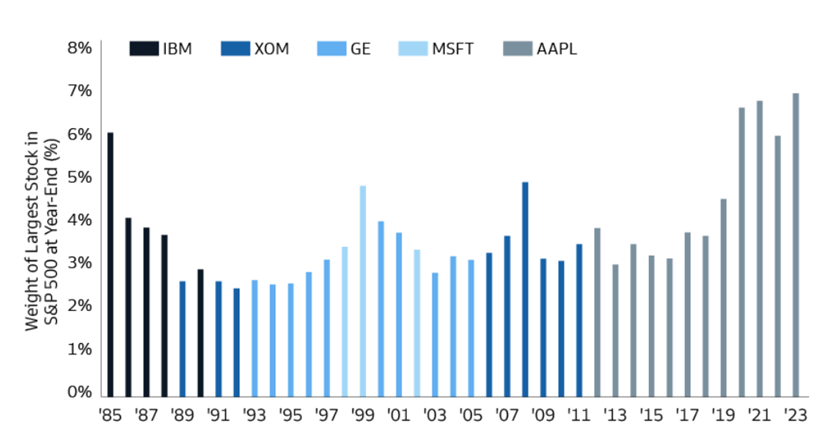

The S&P 500 and growth stocks benefitted from continued strong results from technology companies during 2023. The outsized results of these companies pushed their valuations even higher, with Apple finishing the year as roughly 7% of the S&P 500’s value. This is the largest single weighting in the last 30-years and follows three previous years where Apple represented at least 6% of the S&P 500’s market capitalization. While Apple and six other companies were responsible for the lion’s share of the US stock market’s results in 2023, there are opportunities for broader participation as we head into 2024.

Source: FactSet and Goldman Sachs Asset Management. As of December 31, 2023.

What’s on Deck for January?

Download the December 2023 Market Recap below:

Month in Review

A November to Remember!

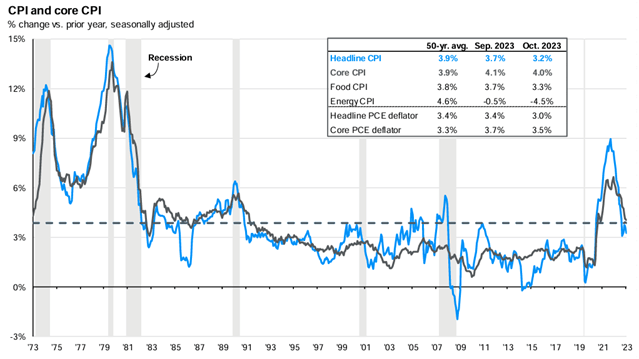

November was a month to remember for investors: The S&P 500 posted its strongest November since 1980 (rising roughly 9%) and the Barclays Aggregate Bond Index had its best month since May 1985 (rising roughly 4.5%).

What were the catalysts for such a sharp reversal?

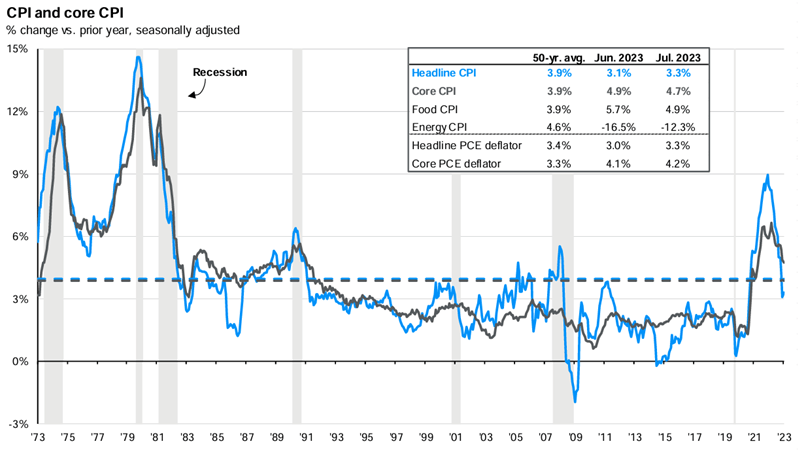

Investor sentiment had become overly negative – a three-month losing streak for stocks and a 5-month losing streak for bonds. This set-up was followed by unexpected positive developments on the fight against inflation. Multiple readings during November showed inflation rising by less than expectations. Federal Reserve officials also affirmed progress towards normalizing inflation, the decline can be seen in the exhibit below. The positive developments on inflation drove interest rates lower, sending stock and bond prices higher, as investors now shift their attention away from rate hikes to rate cuts.

Source: BLS, FactSet, J.P. Morgan Asset Management. CPI used is CPI-U and values shown are % change vs. one year ago. Core CPI is defined as CPI excluding food and energy prices. The Personal Consumption Expenditure (PCE) deflator employs an evolving chain-weighted basket of consumer expenditures instead of the fixed-weight basket used in CPI calculations. Guide to the Markets – U.S. Data are as of November 30, 2023.

What’s on Deck for December?

Download the November 2023 Market Recap below:

Month in Review

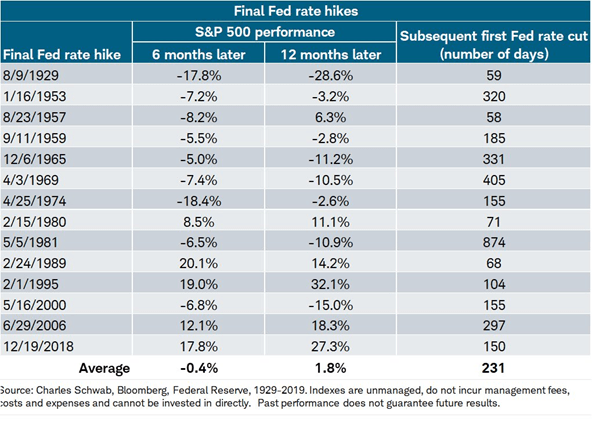

Last Rate Hike? Now What?

The Federal Reserve held its November committee meeting, where they kept interest rates unchanged. Following the press conference, investors are now expecting interest rates to be unchanged again in December (only a 15% probability of a December rate hike as of 11/2/2023). If the Federal Reserve is finished increasing interest rates this cycle, what does that mean for the stock market? Going back to 1929, there are no clear trends, the range of outcomes following the last hike is very wide historically. While various talking heads remain hyper-focused on short-term events such as this, it is more important than ever that investors maintain their focus on long-term fundamentals.

What’s on Deck for November?

Download the October 2023 Market Recap below:

As enthusiasts and collectors approach the later stages of their lives, the act of collecting takes on new dimensions. Some may be content to sell their collection and pass the proceeds on to heirs, but for others the treasures that have been amassed over the years are now an opportunity to leave a legacy that will continue to endure.

Here are four considerations to help navigate this phase of your collecting journey:

If you haven’t already, start to incorporate your collection into your broader estate plan. Decide how your treasures will be managed, preserved, or passed on. Engage with experts who specialize in collectibles and estate management, particularly those well-versed in the tax implications of transferring collections.

Consider which heirs will receive each item and why, taking into account their emotional significance and potential for instilling responsibility. If you aim to establish a philanthropic legacy, donating to a museum or organization aligned with your mission not only offers tax benefits but also ensures parts of your collection remain together.

While financial considerations have likely played a role in your collecting journey, the emotional value of your treasures becomes increasingly significant as you near this phase. Embrace the joy and memories your collection evokes. If the next chapter is one that doesn’t fetch your estate the highest possible payout or the most optimal tax deduction, that can be OK if the destination fulfills your wishes and maximizes the emotional component of the transition.

Consider the broader impact your collection can have. Some individuals opt for philanthropic endeavors that align with the themes of their collection. For example, a collector of classic cars may choose to donate his or her collection to an automobile museum that will display the vehicles and allow them to continue to provide joy for many. Donating items, contributing proceeds to charitable causes, or establishing cultural endowments can solidify your legacy as one that extends beyond material possessions.

Once you’ve established a robust plan for your collection, it’s crucial to have capable individuals ready to carry it out. For vehicles, consider arranging for an appraisal in advance or identify a trusted appraiser to guide those handling your estate. If you anticipate liquidating a coin collection after your passing, take the initiative to identify a reputable precious metals dealer beforehand. By personally selecting the third parties involved, you can alleviate the executor’s potential challenges in managing and distributing your collection.

As your collecting journey matures, it evolves into a narrative of legacy and stewardship. It’s important to recognize that your collection signifies not just an investment, but a testament to the diverse experiences of your life. Take the necessary time and consider that at Confluence Financial Partners, we’re here to help. Collaborating with the right professionals can help ease the burden and ensure both your life and legacy are maximized.

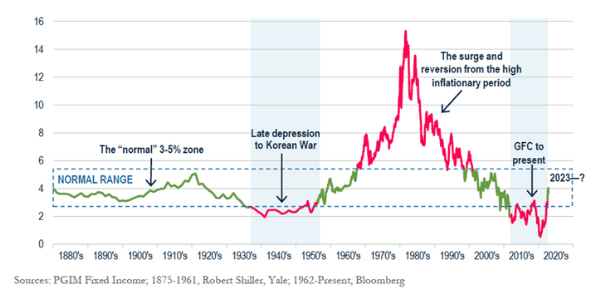

Month in Review

Bond Yields Return to Average

Despite nearly a decade of low interest rates, the 10-year Treasury yield typically averages 3% to 5% yield, going back to the late 1800’s. For the first time since 2007, the 10-year Treasury rose to 4.5%, comfortably returning to long-term averages. Recent inflation data was stronger than expected, contributing to the increase in yield, along with the prospect of additional rate hikes from the Federal Reserve. The increase in yields reduces the value of bond investments in the short-term, and higher yields present a more attractive alternative to stocks – two reasons stocks and bonds struggled in August and September.

What’s on Deck for October?

Download the September 2023 Market Recap below:

Month in Review

Insight on Inflation

Despite the market volatility, evidence from July’s inflation report suggests progress towards a “soft landing” scenario, where inflation is gradually decreasing, and the economy avoids a recession. In July, headline inflation was at +3.3%, year-over-year, down from its peak of 9.1% in June 2022. Unlike June 2022, supply chains and goods have largely normalized, with wages and services being the key drivers of inflation today.

Source: BLS, FactSet, J.P. Morgan Asset Management. CPI used is CPI-U and values shown are % change vs. one year ago. Core CPI is defined as CPI excluding food and energy prices. The Personal Consumption Expenditure (PCE) deflator employs an evolving chain-weighted basket of consumer expenditures instead of the fixed-weight basket used in CPI calculations. Guide to the Markets – U.S. Data are as of August 31, 2023.

What’s on Deck for September?

Download the August 2023 Market Recap below:

Our mission at Confluence Financial Partners is to Maximize Lives and Legacies.

As our industry has evolved, we understand that the role of a wealth management firm has become bigger than simply managing portfolios and building financial plans. While plans and portfolios remain essential, we believe that true wealth lies not only in financial abundance but also in physical and mental well-being. Studies show that individuals who prioritize their health tend to experience enhanced cognitive function, increased productivity, and overall improved quality of life.

In light of this, it is with much enthusiasm that we announce the addition of a dietitian to our team at Confluence, Sarah Rupp, MS, RD, LDN!

Our commitment to associates and clients is to expand beyond the conventional boundaries of wealth management and we believe the addition of Sarah helps us deliver that commitment.

We look forward to sharing Sarah’s knowledge to further Maximize Lives and Legacies.

Great Days Ahead!

Greg Weimer, CEO

The banking system recently became front-page news following the failure of two banks in March. The headlines related to bank failures can illicit very emotional responses about safety of deposit accounts and cash investment solutions.

Cash management fundamentally breaks down into two categories:

While the two have similarities, there are fundamental differences with structure and protection.

In addition to FDIC insurance and backing of the full faith and credit of the US government, most assets held at firms such as Raymond James are covered by the Securities Investor Protection Corporation (SIPC), to applicable limits. The SIPC was established in 1970 and protects client assets up to $500,000, including $250,000 of cash. SIPC account protection would apply in the event a firm fails financially and is unable to meet obligations to clients, not against a loss in market value.

Despite the negative and unsettling headlines, there are multiple robust cash management solutions available to clients, with multiple layers of risk mitigation. At Confluence Financial Partners, we believe in the soundness of our banking system and maintain complete confidence in our client cash management tools.