Articles

Stock Market Recap: July 2024

Month in Review

Equity Market Rotation

Last month’s monthly update discussed the record levels of concentration in the S&P 500 – a factor that likely played a role in the significant shift equity markets saw in July.

After the June inflation (CPI) report was released, investors shifted expectations to a much higher likelihood of a rate cut in September. Generally, small cap stocks have a greater sensitivity to interest rates, given the use of more floating rate debt compared to large cap stocks. This factor, combined with improving earnings fundamentals, resulted in the Russell 2000 outperforming the NASDAQ by over 5% the day of the inflation report. This represents the largest single day outperformance of small cap stocks versus technology stocks in over 40-years (chart below)

Source: JPMorgan Asset Management, Bloomberg, as of July 21, 2024

Small caps kept up the momentum of July, along with large cap value stocks (Russell 1000 Value TR Index, +5.11%).

July represented an important reminder to long-term investors about the benefits of maintaining a diversified approach

What’s on Deck for August?

Although many of us have good intentions when it comes to prioritizing physical, mental and emotional health, the necessary action of consistency with establishing new habits to support these categories doesn’t just happen overnight.

Most of us can identify areas in our daily routines that need improvement. However, factors such as energy levels, time and effort required, childcare availability, and finances can present significant obstacles to making beneficial changes. As a result, most of us continue on the path that works “well enough” for the short term, even if it’s not ideal. The issue typically isn’t a lack of desire or knowledge to make changes, but rather the absence of a conducive environment for these changes to take root and flourish. In other words, a space needs to be created for change to happen.

Take healthy eating for example. It’s something you know you want to do more consistently, it’s something you know would be beneficial to your short and long term health, but you can’t seem to bring yourself to take inventory of your fridge and pantry to begin to stock quality items in your home, to set yourself up for success. Or maybe preparing food is a barrier. You have access to cooking and food prep videos and articles at your fingertips, but where in your schedule have you created time to prepare then execute actually trying it yourself?

Peeling back the layers on why good intentions don’t necessarily translate to actions can be painful and humbling. It’s caused many of us to stay stuck in the same place, in different areas of our lives, for a long time. So, what’s the solution?

It’s time to stop fooling ourselves that changes just happen without our concentrated effort. If we fail to plan, we plan to fail. Once evaluated that a certain tweak/change would be advantageous, it’s time to take the step to create the structured space in the schedule where a new habit can take root. Keep it simple. Narrow the focus. Most of us are juggling many “glass balls” that we cannot afford to drop and have shattered. An example of this would be personal health, which too often can be put on the backburner for a time period out of practical necessity, but where does this lead to in the long run? Consider this encouragement to start where you are.

Here are some tips for getting started:

1. Identify. What is really frustrating you about your daily or weekly routine? Frustration is a driver to change. Be specific here. If you just focused on what was frustrating and what would make it less frustrating/better, what would it be?

2. Reserve. Pick a time in your schedule and dedicate yourself to education (self-education through reading, watching how-to videos, podcasts, in person professional help), as you prepare to make a change.

3. Clarify. Write down a clear goal and put it somewhere you can see it daily, as a reminder to yourself.

4. Take Action. Go and do it! It’s time to execute rather than thinking about it anymore!

5. Practice this for small habit changes or big habit changes. Enlist accountability people as desired. Pat yourself on the back for taking a step of action.

My goals may differ from yours, and in fact, they likely do, spanning personal to professional aspirations. However, the implementation of self-discipline to commit to change and adapt to new ways of living will likely positively impact all areas of your life.

“If you talk about it, it’s a dream, if you envision it, it’s possible, but if you schedule it, it’s real”. Let’s have less talk, more scheduled action and a space created for ourselves to actually adopt behavior change. Cheering you on today!

Disclaimer: This article offers educational insights from a registered dietitian on establishing healthy principles. It is a supplementary resource and not a substitute for personalized advice from a medical professional familiar with an individual’s health history.

Label reading, ingredient decoding, deciphering marketing terminology – all of these aspects individually or combined can create an environment of confusion for shoppers at the grocery store. Amongst product labels, “USDA Organic” is found on many foods and beverages, but what does it really mean? Let’s focus in and unpack this particular label.

The United States Department of Agriculture (USDA), is a division within the US government that focuses largely on the country’s safety and efficiency of farming, food and sustainability practices. The USDA Organic label is federally regulated, meaning the product its placed upon has met the standard requirements to earn the status of this particular label (more on this, below). Because this is a regulated label with strict criteria, the consumer can have confidence when they see this symbol on a product that the process in which the ingredients have gone from farm to table has been verified through a system of checks and balances.

These standards are in place to ensure both the consumers and environment are set up for better health outcomes, given how products are grown and processed. More information surrounding these categories can be found on the USDA website.

If a food product does not have this label, the default is known as a conventional food. A conventionally grown product such as a head of broccoli, for example, could miss the mark for organic in a minimum of one category or at most, all categories. Conventional foods are found in most products in store and have their own system of checks and balances for consumer health, as well.

Whereas conventional foods are still federally monitored for safe limits of pesticides using scientific data and risk assessment on a regular basis, these types of products do not have to meet as rigorous requirements surrounding chemical usage on crops and soil health, for example. Additionally, they may utilize GMO’s, and/or differ in the treatment of animals and farming practices.

In summary, organic verified products have tighter regulations when it comes to how a food is grown and processed, and also how animals are fed and raised. Common concerns from consumers regarding conventional foods vs. organic surround long term pesticide intake risk on human health, animal welfare, and the question of varying levels of nutrient composition. Given the increased cost of production to farm organically, organic products most often have a higher price tag than their conventional counterparts. Many believe there are benefits to choosing organic, but it may not be necessary or realistic to consume all or even most food intake organic, depending on food budget and/or availability of items where someone lives and shops on a regular basis.

When it comes to a measurable benefit to human health, choosing organic foods vs. conventional, the scientific evidence is not definitive, although observational studies point to better health outcomes over time for organic consumption vs. conventional². Like any decision in the adult world, the type of food you purchase requires taking inventory of what you value, prefer, and can afford.

If at this point you’ve identified you’d find it worth the money and efforts to choose organic, in some capacity, for yourself and family, it can be helpful to have a simple starting point.

Each year, the Environmental Working Group (EWG), a non-profit organization whose focus is public health and the environment, releases two lists – the dirty dozen and clean fifteen. These lists are considered “shopper’s guides” for the consumer who wants to better understand which foods have been tested and shown to have a greater amount of pesticide residue (dirty dozen) compared to produce with less or no traces of pesticides (clean fifteen). This is a great place to begin for a consumer who desires to limit pesticide residue on food they’re consuming, due to potential health risks associated with chemical exposure for adults and children, alike.

2024 Dirty Dozen³ – EWG recommends to buy these organic, when possible, to avoid concentration of pesticides:

2024 Clean Fifteen⁴ – EWG reports least contaminated with pesticides, among produce tested. OK to buy conventional:

You can request a copy of these lists from the EWG website, print them out for your fridge or screenshot them for your next trip to the grocery store. You can also take a deeper dive to learn more about the EWG’s process for food testing on their website.

When it comes to eating nutritiously by principle, it’s best to consume whole foods, as close to natural form as possible, and a variety of types within each food group (fruits, vegetables, fats, proteins, whole grains, dairy). If a fixation on choosing organic vs. conventional is presenting as a hindrance from eating animal products or produce, that may be missing the point for what healthy eating actually looks like. The term organic isn’t necessarily synonymous for better health, so it’s important to view the whole picture.

As a consumer, it’s important to be aware of common food labels such as “USDA Organic” on products like meat, dairy, fruits, vegetables, eggs and other processed foods. Understanding what the term implies can assist in avoiding conflicting information and confusion, in this area. The choice of conventional vs. organic is yours, and it’s a personal one. My hope is that you feel better acquainted with the facts and are empowered to make your choices with confidence!

Sources:

Disclaimer: This article offers educational insights from a registered dietitian on establishing healthy principles. It is a supplementary resource and not a substitute for personalized advice from a medical professional familiar with an individual’s health history.

As the end of the year approaches, it’s an opportune time for clients to utilize strategies that align charitable goals with their financial objectives. In this article, we will explore various charitable planning opportunities and strategies to leverage to help our clients optimize their giving while improving their overall financial situation.

Tax Efficient Charitable Giving Opportunities

One of the primary incentives for charitable giving is the potential to reduce taxable income. However, timing and method play a crucial role in maximizing these benefits. Below are several techniques to consider as part of year-end planning:

Donating Appreciated Securities: Instead of giving cash, clients can donate appreciated stocks, bonds, or mutual funds directly to a charity. This strategy offers two key benefits:

Qualified Charitable Distributions (QCDs): Clients aged 70½ or older can make a QCD of up to $105,000 annually (indexed annually to inflation) directly from their IRA to a qualified charity. QCDs offer several advantages:

Bunching Charitable Contributions with Donor-Advised Funds (DAFs): Since the introduction of higher standard deductions through the Tax Cuts and Jobs Act (TCJA), many clients no longer benefit from itemizing deductions annually. Bunching donations into a single year can help overcome this threshold. Bunching involves concentrating charitable giving into one year to surpass the standard deduction, allowing clients to itemize and maximize their tax savings.

One way to implement this is through a Donor-Advised Fund (DAF):

Charitable Trusts: Charitable trusts are powerful tools for individuals looking to balance their philanthropic goals with tax-efficient wealth management. These trusts not only provide a way to support meaningful causes but also offer substantial tax benefits for donors and their heirs.

Incorporating Family in Charitable Planning

Holiday gatherings present a unique opportunity to engage family members in philanthropy. Clients can involve their children or grandchildren in charitable discussions to foster shared values and create a lasting legacy of giving.

It’s important to manage expectations on how the family will work together; make it optional, not mandatory, to create the most positive experience possible. You should also honor individuality and allow your children the flexibility to choose the organizations they want to support; involving adult children in the decision-making process is vital, but it will be frustrating to them if they feel like they are only along for the (your) ride.

Charitable giving shouldn’t be compulsory because it immediately becomes an obligation as opposed to enjoyable. Finally, giving small gifts to every organization that asks each year might be easier than saying no, but to truly maximize your legacy, try to create a plan to give to charitable organizations in such a way to create a big change.

Maximizing Impact with Matching Gift Programs: Clients should check if their employers offer matching gift programs, which amplify the impact of charitable donations. Many companies will match employee donations dollar-for-dollar, effectively doubling the contribution. Some corporations also match volunteer hours, allowing clients to combine their time and financial resources for greater impact. Encouraging clients to investigate these programs can result in more strategic giving.

Creating a Year-End Giving Plan with Your Wealth Manager

Your wealth manager can help you formulate a personalized year-end charitable giving plan. Here’s a checklist approach to developing it:

By using strategies such as donating appreciated securities, leveraging QCDs, or utilizing donor-advised funds, clients can maximize both the impact of their giving and the financial benefits. Incorporating charitable planning into family discussions further deepens the impact while fostering a legacy of philanthropy. As the year draws to a close, now is the perfect time for clients to engage with their Wealth Managers in conversations about their charitable goals and ensure they have a plan in place.

Month in Review

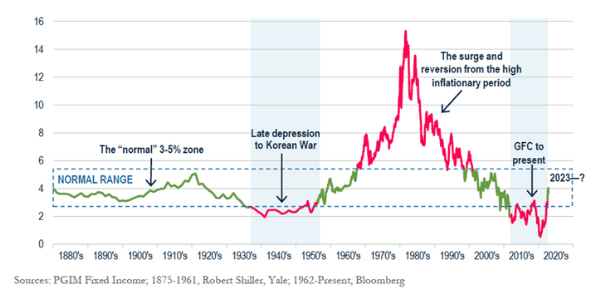

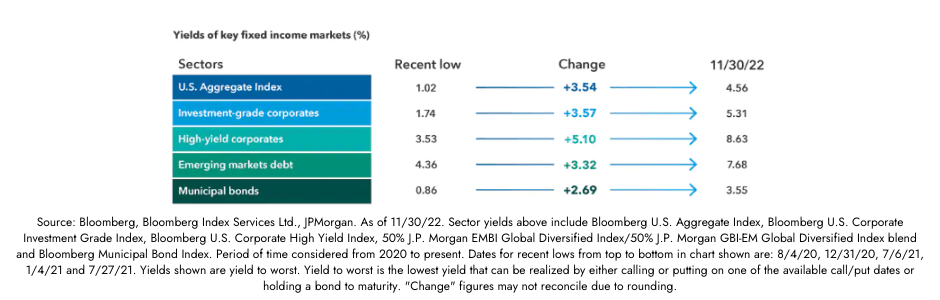

Bond Yields Return to Average

Despite nearly a decade of low interest rates, the 10-year Treasury yield typically averages 3% to 5% yield, going back to the late 1800’s. For the first time since 2007, the 10-year Treasury rose to 4.5%, comfortably returning to long-term averages. Recent inflation data was stronger than expected, contributing to the increase in yield, along with the prospect of additional rate hikes from the Federal Reserve. The increase in yields reduces the value of bond investments in the short-term, and higher yields present a more attractive alternative to stocks – two reasons stocks and bonds struggled in August and September.

What’s on Deck for October?

Download the September 2023 Market Recap below:

Month in Review

What Happens Next: Soft or Hard Landing?

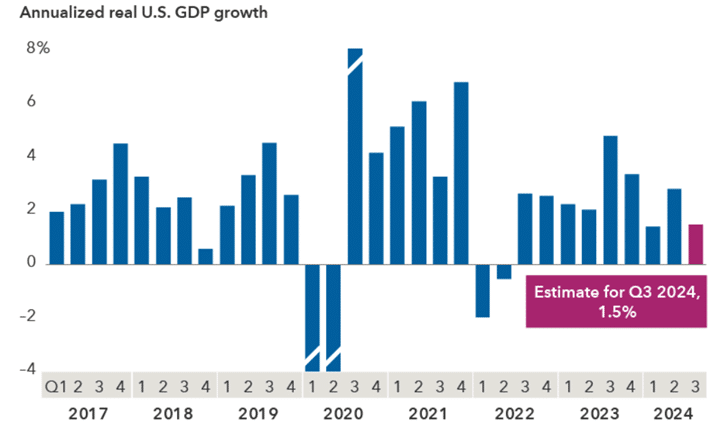

The Federal Reserve is poised to cut interest rates in September, the first interest rate cut since they began increasing interest rates in March 2022. Investors are now pondering, “what happens next?”: a “soft” or “hard” landing for the economy.

While not officially defined, a soft landing would be a continued decline in inflation and interest rates, without growth slowing down enough to enter a recession. Hard landing would be the opposite – a continued increase in unemployment and a slowdown in economic growth, resulting in a recession. Soft landings are historically less common, with the most recent (and classic case) being the 1994-1995 period.

Inflation has fallen closer to the Federal Reserve’s target rate, while unemployment has also begun to increase, prompting the likely rate cut in September. However, other signs indicate continued strength in the economy: for example, estimates for GDP growth this quarter stand at +1.5%. With no clear forecasts for a soft or hard landing, investors have priced in three to four rate cuts by the end of 2024, indicating expectations that the Federal Reserve will start and continue rate cuts in September.

Sources: Capital Group, Bureau of Economic Analysis, FactSet. Figures for Q1:20, Q2:20, and Q3:20 are –5.5%, –31.6%, and 31.0% respectively, and are cut off by the y-axis given the extreme fluctuations associated with the COVID-19 pandemic. Estimate for Q3:24 is based on the mean consensus estimate from FactSet. As of August 22, 2024.

What’s on Deck for September?

We’ve all heard the numbers. Over the next 30 years, an estimated $70-$90 trillion is going to pass from the Baby Boomers to the next generation. This will be a transfer of wealth the likes of which the world has never seen. Not only are the Baby Boomers the wealthiest generation ever to live, their wealth is broad and relatively spread out. Generally speaking, this is the first generation in which the middle class will play a significant role in the wealth transfer. While Boomers’ parents largely had pensions that ended at death, their children instead have sizable retirement accounts that will be passed down. Add that to the fact the American and global economies have massively expanded over the past 50 years, and we have a recipe for a wealth transfer for the ages.

At Confluence Financial Partners, our mission is to help our clients maximize their lives and legacies. When it comes to legacy, the upcoming wealth transfer is an important issue for the majority of our clients. That means that a major part of our job is to help our clients, where appropriate, engage the next generation in hopes that the family legacy will continue. Studies have shown that 70% of families lose their wealth by the second generation, and 90% by the third. We want to help families avoid being part of this statistic, and instead build something that lasts.

Here are four steps that you can take to help ensure that your legacy is secure.

Consider a Multi-generational Advisory Relationship

Over 50% of our clients are multigenerational, meaning we have family members in more than one generation who we are serving. Often children are clients with their parents from a young age, but as they become adults, they become more independent and establish their own relationship with us as their advisor. Another common situation is when clients refer their parents to us, forming a multigenerational relationship from the other direction. Still another way this happens is when adult children establish a relationship with us as their parents (who are clients already) age and it becomes even more important to all be on the same page.

Even if you are not a Confluence client, we would encourage you to find an advisor and a firm that is making multi-generational wealth considerations a priority. Your advisor should help you bridge the gap between the wealth that you’ve built and the next generation for whom you hope that wealth will be a blessing. We have shepherded many families through this difficult period already, and the whole process is undoubtedly much easier if the parents and the children share the same advisor.

Take Another Look at Your Estate Plan

When was the last time you had your estate plan reviewed? If you are like most Americans, it’s probably been a few years. The typical estate plan is adequate for only a certain season of life, and it will need to be redone as children get older and circumstances change. Like a financial plan or an investment portfolio, an estate plan should be periodically updated as goals change. An estate plan update is almost always needed after a major life event such as a birth, a death, or a change in marital status.

Sometimes an estate plan can be as simple as a pair of wills and power of attorney documents. More often, however, trusts should be involved and more careful consideration should be taken to help ensure that wishes are carried out. For example, what would happen in the event of a death or divorce of a child? If protections aren’t built into the estate plan, it’s possible that a parent’s wealth ends up with a child’s ex-spouse instead of the grandchildren. That is an avoidable scenario, but it’s important to ask the right questions and think critically about the key factors that will cause the plan to either be successful or not.

We don’t have attorneys at Confluence, but we do have a robust process for reviewing your existing estate plan so that you understand your current situation. Once we learn where you are today, we can help educate you so that you are prepared when you speak to your attorney about updates. We work closely with our clients throughout the whole process and are there to help in every way we can.

Communicate, Communicate, Communicate

The primary reason that the wealth transfer could go poorly for the majority of families is a lack of communication. An inheritance can be a difficult subject to broach, especially for the first time. As a result, many families put these conversations off until it is too late. Don’t let that be your family.

We find that most families assume that their children will handle the inheritance with ease, but that isn’t always the case. We’ve seen many situations in which the heirs were paralyzed by their newfound wealth and the responsibility that comes along with it. They don’t feel prepared to handle the wealth, and so it wears on them. Rather than enjoying the legacy that their parents worked so hard to build, they instead live in fear of losing it all. Fortunately, this can be remedied by simple and consistent communication. Imagine if those same heirs had been let in on the family wealth along the way. Imagine if they knew how the accounts and estate plan were structured. Most importantly, imagine if they understood their parent’s dreams and wishes around the wealth. Imagine they understood the values and expectations that go along with the wealth being transferred.

One question we often ask our clients is this: Will your children still speak to each other after you are gone? Many clients take this for granted, but an estate plan that has not been communicated will inevitably lead to disagreements and fraught relationships. This is especially true in unique situations where the split is not even amongst the heirs, but money can cause even the most reasonable people to turn their backs on each other. Thankfully, again the odds of this happening can be greatly reduced with solid and consistent communication on the part of the wealth creators. Don’t leave ambiguities that can be interpreted. Make your wishes known and take the (sometimes) uncomfortable step of starting a pattern of communication.

Have a Family Meeting

One concrete way to start or solidify communication around the great wealth transfer is to have a family meeting. Ideally, this would lead to a regular cadence of meetings, but the first one is usually the hardest. These meetings can take many different forms, but they are typically initiated by the wealth creators of the family and include the adult children in the upcoming generation. Many families want to communicate better about important topics like their estate plan, financial expectations, and charitable goals, but they don’t know where to start. That’s where a family meeting can be a great opportunity to open important lines of communication.

At Confluence, facilitating these family meetings is one of the most important things that we do. We regularly sit down with our client families at our office or their homes to help get everyone on the same page. We don’t believe this type of meeting should be only done in an emergency after a terminal diagnosis, although that may sometimes be necessary. Rather, we think it is essential to start thinking about this now, before there is a crisis of any kind. Communication around wealth transfer that is done while the whole family is focused and not in crisis is ideal because it prepares the family to be ready if or when the crisis does arrive.

Conclusion

The largest wealth transfer that the world has ever seen is coming. For many, it has already started. That transfer is going to go well for some families, but very poorly for many. At Confluence, we’ve made the next generation a priority, right down to the way we have structured our firm. Many advisors work as lone wolves, with no real succession plan or assurance of what will happen to the families they serve once the advisor retires. At Confluence, we are building a firm so that we can help not only our current clients, but their children and grandchildren as well. We work in teams, and we have advisors who are in their 70s all the way down to their 20s. We’ve made significant investments in growing the next generation of advisors so that our clients’ children and grandchildren can be confident in the Confluence of the future.

As you read this today, we implore you to start thinking about what your next step may be towards making sure that your financial legacy is secure. Perhaps you need to have your estate plan reviewed, or you should make that call to your attorney that you’ve been putting off. Maybe you’ve been meaning to ask your advisor about a family meeting or considering introducing your parents or children to your financial team. Whatever the next step is for you on this journey, we ask you to take it. Your family will be grateful that you did.

Confluence Wealth Services, Inc. d/b/a Confluence Financial Partners is a SEC-registered investment adviser. Confluence Financial Partners only transacts business in states where it is properly registered or notice filed or excluded or exempted from registration requirements. The security of electronic mail sent through the Internet is not guaranteed. All email sent to or from this address will be received or otherwise recorded by the Confluence Financial Partners corporate email system and is subject to archival, monitoring and/or review, by and/or disclosure to, someone other than the recipient. Confluence Financial Partners recommends you do not send confidential information to us via electronic mail, including social security numbers, account numbers, and personal identification numbers, unless properly encrypted. A copy of our current written disclosure statement discussing our advisory services and fees continues to remain available for your review upon request or by visiting the following link:https://www.confluencefp.com/form-adv-2a/

You can do well by doing some good! Not only can giving to a charity make a positive impact, it can provide an opportunity for some tax benefits too. If you are a high-income earner or a retiree who plans on writing checks to your favorite charities, then you may benefit from these three wealth and tax planning tips you can take advantage of in the future.

In Summary

Act today and consult your fiduciary wealth manager and tax professional to develop a plan to best align with your goals and charitable endeavors. You have an opportunity to make a positive IMPACT on charities both today and tomorrow while also receiving some tax benefits along the way. Please do not hesitate to contact us if you have any questions or if we can help in any way.

Heading into 2023, the Investment Advisory Committee believes we are beginning to return to a more historically normal, rational economic environment.

The Committee has identified four key themes for 2023 and the years ahead:

Source: Morningstar

The future is impossible to predict, and nobody has a crystal ball. However, we believe that the four themes listed above will likely have a major impact on investor outcomes over the next year and beyond.

If you would like to talk through how these themes may impact your portfolio, please give us a call.

Working with a Registered Investment Advisor (RIA) is desirable for high-net-worth individuals, families, and institutions for the personal, unbiased, and tailored advice to their unique financial situation. They have a fiduciary duty to act in your best interest while providing comprehensive financial services to meet your goals.

A Registered Investment Advisor is a firm registered with the Securities and Exchange Commission (SEC) that provides clients with financial advice. A team of advisors will often employ their expertise for customized guidance with the freedom to choose from a wide range of investment options for tailored advice for you.

The fiduciary standard of an RIA has a “fundamental obligation” to work in the best interests of its advisory clients. Recommendations will be made in good faith, based on your needs, and allow a direct line of communication if there is a need for clarification or change.

Financial professional teams within an RIA firm are often skilled in disciplines beyond just portfolio management. They include retirement, estate, charitable legacy, tax, insurance, education planning for you and your family, and corporate services, including employee benefits. These teams will work hand-in-hand with an established financial network to develop investment strategies considering tailored solutions for your unique financial situation.

Each RIA must file and publicly post a Form ADV that offers a comprehensive view of the organization. A Form ADV offers objective and transparent information, including conflicts of interests, compensation, disciplinary filings, education, and the firm’s key personnel.

Many RIA’s offer financial advice and planning for a fee based on a percentage of your assets under management. This service creates a mutual benefit of a transparent fee structure that aligns the clients’ best interests with those of the RIA.

Many wealth management teams will usually include highly experienced financial professionals with prestigious designations. These teams often bolster professional training and certifications such as the Certified Financial Planner® (CFP®) designation, Accredited Asset Management Specialists® (AAMS®), Certified Public Accountant (CPA) or Accredited Investment Fiduciary® (AIF®) and commit themselves to continuous education on your behalf.

Simple, straightforward, and non-biased assistance with your comprehensive financial plan aligns with the priorities of an RIA. If you are looking for wealth management advice at a concierge level of service, Confluence Financial Partners, may be the team of financial professionals for you.

Please contact a member of the Kimmich Team if you’re interested in having a discussion.