Month in Review

- Value and international equity markets continued their strength in February, extending the strong start to 2026 for diversified portfolios.

- The S&P 500 TR Index declined -0.76% for the month, with technology and growth stocks again weighing on the index. Large cap growth stocks declined -3.36% in the month of February, taking 2026 returns to -4.82% (Russell 1000 Growth TR Index)

- Equities outside of large cap growth again showed strength. Within the large cap space, value rose +2.59% in February (Russell 1000 Value TR Index), small caps rose +0.80% (Russell 2000 TR Index), and international equities led major equity indices at +5.02% during the month (MSCI ACWI Ex-USA NR USD Index)

- Bond markets benefitted from a decline in interest rates across the yield curve, driving the core bond index to a strong +1.64% monthly gain (Bloomberg Barclays US Aggregate Bond TR Index)

Stock Market & Geopolitical Events

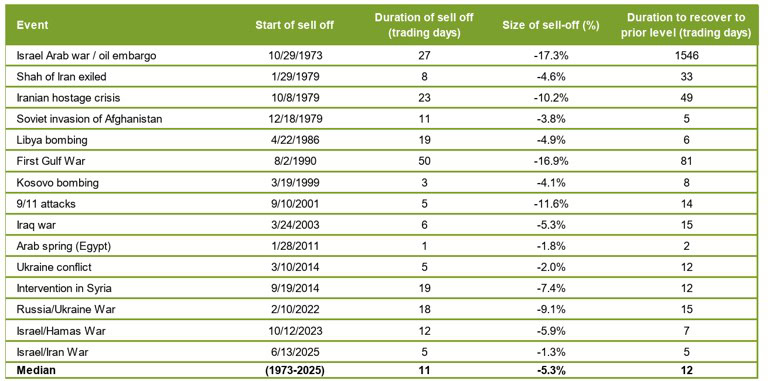

One of the more well-known investing adages is the “stock market climbs a wall of worry”, which is particularly appropriate for times of geopolitical conflict such as the present.

Acknowledging the human impact of geopolitical events, history shows that the impact to equity markets tends to be short-lived. Looking at the period since the S&P 500 was incepted, excluding the present conflict in Iran, the S&P 500 has declined an average of -5.3% over 11 trading days following the start of major geopolitical events (shown in the table below).

Historically following the initial sell-off, investors digest the fundamental impact to the stock market (which tends to not be long-lasting in nature), and the stock market exhibits some symmetry – recovering the initial loss in an average of 12 trading days. While conflicts like the present can exhibit immense human cost, history shows that the stock market will continue to climb the wall of worry.

S&P 500 Selloffs Around Geopolitical Events

What’s on Deck for March?

- The Federal Reserve meets on March 18th, but as of the time of writing, investors are pricing in a 97% probability of no interest rate cuts. Current pricing indicates expectations of two 0.25% rate cuts in 2026.

- Following earnings season, expectations for capital expenditures on AI technologies reached new extremes. The five “Hyperscalers” (Amazon, Alphabet, Meta, Microsoft, Oracle) have guided roughly $700bn of capex in the next 12 months. If realized, this would be one of the larger investment outlays relative to GDP in modern history (~2% of GDP). Investors are paying close attention to efficacy of this record investment.